Title insurance is oftentimes one of the more expensive closing costs for home buyers, yet many are not quite sure what they are paying for. While purchasing a policy is certainly a necessary expense for any property owner, it is important to understand the various factors that impact the pricing and which ones may help you save money.

In this article, our ANSTitle agents will discuss the cost of title insurance and what’s included in the premium you pay. We will also explain the value of having title insurance and share some tips on how to save money when shopping for a new policy. Â

Title Insurance Cost in Regulated States

In Florida, Texas, and New Mexico, the title insurance rates are set by the state insurance department and all agents are required to charge the same premiums. While each of these states uses a different calculation to determine the exact rates, in all three the title insurance premium grows proportionally with the price of the property.

If we look at Florida, the premiums are based on a rate per $1000 of property value and the rate per $1000 decreases as the overall property value goes up in tiers. For example, the title insurance cost for a $250k Florida home would be calculated at $5.75 per $1000 for the first $100k, plus $5.00 per $1000 for the remaining $150k.

There are a number of web-based calculators that can help you estimate the title insurance premium for a home in one of the states we mentioned in this section.

Title Insurance Cost in Unregulated States

Most states don’t impose any regulations on title insurance premiums and in those locations rates can vary widely from one agent to the next. If you are purchasing a home in an unregulated state, you should get quotes from a few title insurance companies in order to get the best deal.

Remember, however, to also review the agent’s online reviews and ratings. If an unexpected title claim is ever brought against the property, you would want to have a solid company by your side that will help you through the process. While selecting the cheapest title insurer may be tempting, it may end up costing you more in the long run. Â

Endorsements and Other Expenses

In addition to the basic title insurance premium, you may also have to pay fees for various property and mortgage endorsements, title search, land surveys, settlement and recording fees, and more. Depending on the state you’re in, these items may be itemized or all the fees may be bundled together into one price.

Our agents can help you determine which additional fees would be required for your policy and provide a more accurate estimated total.

Regardless of whether your property is located in a state that regulates title insurance or not, you should expect to pay a premium equal to about 0.5% to 1% of the property purchase price for a lender’s and owner’s policy bundle.

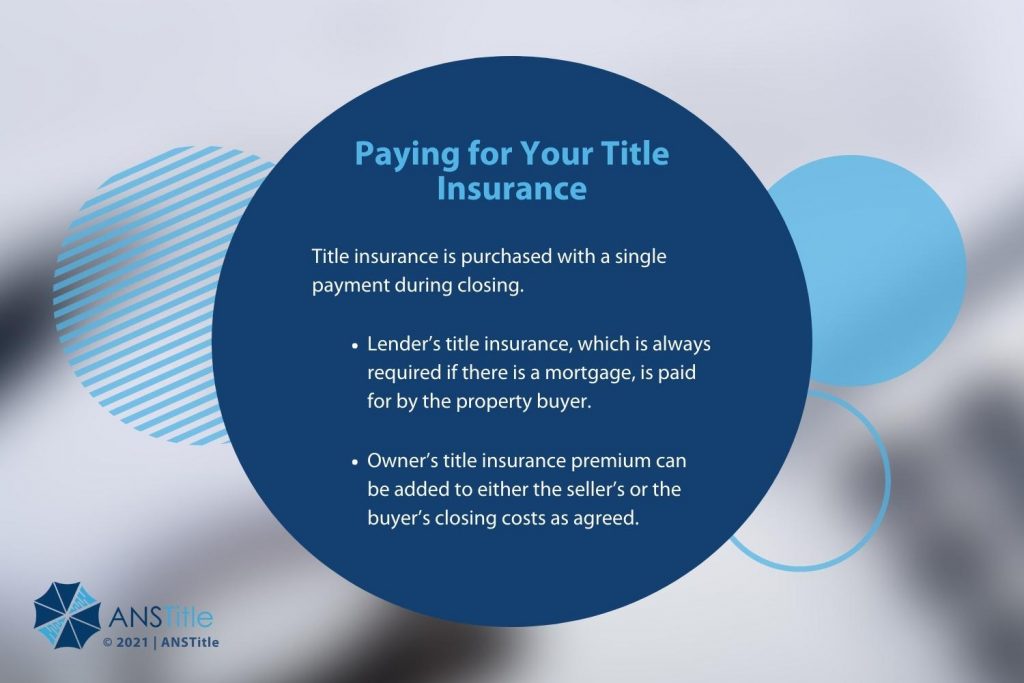

Paying for Your Title Insurance

Unlike most types of insurance, which require monthly or annual premiums, title insurance is purchased with a single payment during closing. The lender’s title insurance, which is always required if there is a mortgage, is paid for by the property buyer.

The owner’s title insurance premium, on the other hand, can be added to either the seller’s or the buyer’s closing costs as agreed upon during negotiations. Â

How to Save Money on Your Title Insurance

If the property you are trying to purchase is located in a state where the title insurance premiums are unregulated, you should take the time to shop around. As we mentioned earlier, the cost of title insurance can vary from one agent to the next and you can easily save hundreds by simply taking the time to request quotes from a few additional providers.

Some other ways that you can lower your title insurance costs include:

- Bundle policies for a discount: if you are taking out a mortgage to purchase the property, you will need to pay for a lender’s policy in addition to the owner’s title insurance. Many agents offer discounts to customers who purchase both policies together.

- Negotiate the property price: Haggling with the seller over the price of the home can not only save you thousands, but it can also lower your title insurance cost since the premium is calculated based on the property price.

- Negotiate the closing cost responsibilities: While in many states it is customary for the seller to pick up the cost of the owner’s title insurance, that’s not always the case. Many sellers, however, will be happy to pay for the title insurance premium to expedite the sale of their property.

- Review the add-ons: As we mentioned earlier, title insurance premiums almost always include additional fees. Work with your agent to ensure there are no unnecessary endorsements and other fees tagged on to your rate.

- Ask for a “reissue†rate if refinancing: if you’re simply refinancing your property, you most likely already have an active title policy. Since the title research is already completed, your agent could offer you a highly discounted premium, sometimes called a “reissue†rate, to keep your business. Â

The Value of Title Insurance

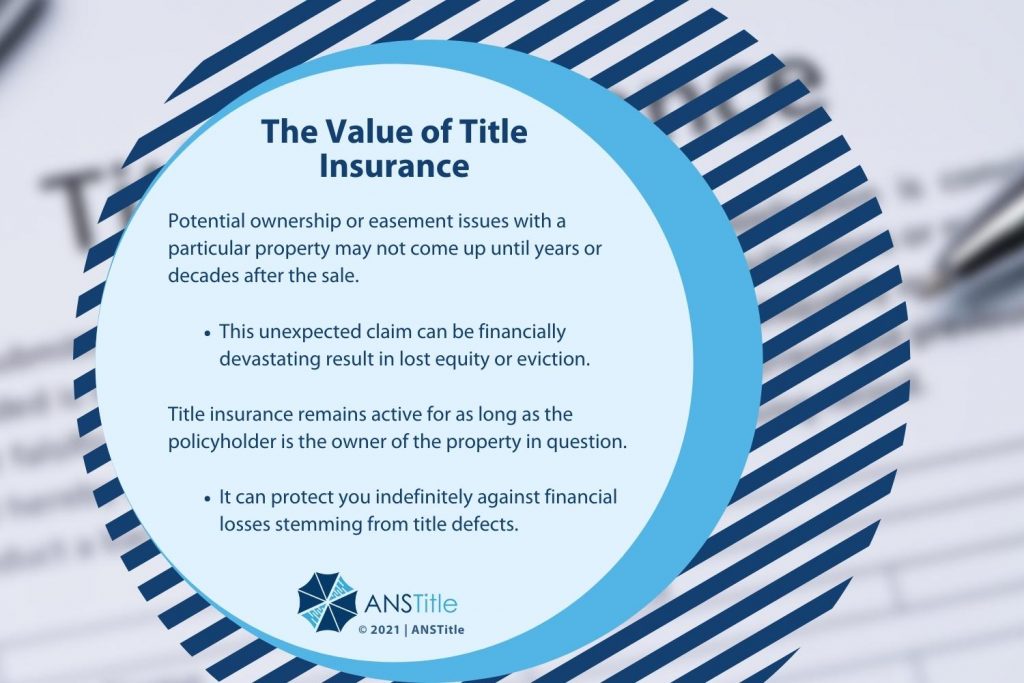

Many homebuyers are lucky and never have to use their title insurance policy to mitigate a title claim. While for those individuals title insurance may feel like a waste of money, paying the one-time premium for it is worth the money. Sometimes potential ownership or easement issues with a particular property may not come up until years or decades after the sale. Such an unexpected claim can be financially devastating for an unprepared owner and result in lost equity or eviction.

Once purchased, title insurance remains active for as long as the policyholder is the owner of the property in question. It is a sound investment that can protect you indefinitely against financial losses stemming from title defects.

If you’d like further information on title insurance pricing for your state, or you’re ready to request a quote, contact one of the ANSTitle agents today. We have over 50 years of experience in the industry and can handle closings in any U.S. location.